Now Reading: GenNext less focused on building firms: Uday Kotak

-

01

GenNext less focused on building firms: Uday Kotak

MUMBAI: Veteran banker Uday Kotak has warned that India’s financial ‘animal spirits’ are fading as the following era of enterprise households focuses extra on managing investments than building and working firms.

Kotak additionally known as for a cohesive technique from policymakers to counter the “vacuum cleaner” impact of US insurance policies, that are pulling international capital away, straining the present account, and affecting the alternate charge and liquidity.

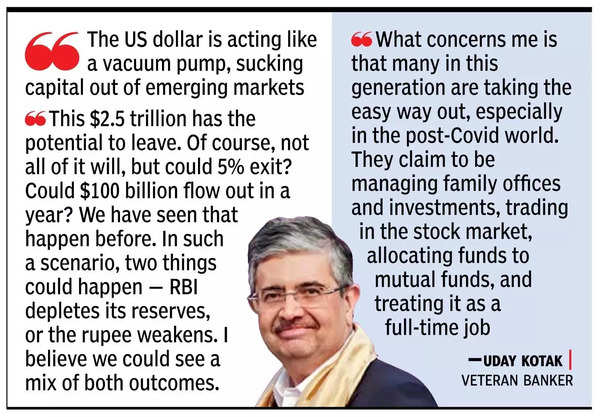

Speaking on the group’s flagship investor occasion, Chasing Growth 2025, he stated, “What concerns me is that many in this generation are taking the easy way out, especially in the post-Covid world. They claim to be managing family offices and investments, trading in the stock market, allocating funds to mutual funds, and treating it as a full-time job.”

He added, “If someone has sold a business, they should be thinking about starting, buying, or building another business. Instead, I see many young people saying, ‘I’m running my family office.’ They should be creating real-world businesses. Why not start from scratch?,” he stated.

While acknowledging the significance of startup funding, Kotak questioned why people at 35 or 40 weren’t contributing immediately. “I would love to see this generation be hungry for success and build operational businesses. Even today, I firmly believe that the next generation must work hard and create businesses rather than becoming financial investors too early in life.”

Kotak additionally highlighted the dangers of comparatively excessive inventory valuations in India. “Should we continue encouraging retail investors to keep buying? Retail investors in India are funnelling money into equities daily, contributing to domestic institutional flows. Money from individuals from Lucknow to Coimbatore is flowing to Boston and Tokyo,” he stated, noting that international firms had been profiting from excessive valuations to ebook income and repatriate funds.

“The US dollar is acting like a vacuum pump, sucking capital out of emerging markets,” Kotak stated, pointing to the influence of a strengthening greenback and rising US Treasury yields above 4.5%, that are drawing capital from world markets. Indian inventory valuations stay considerably larger than these in most different world markets.

India’s exterior account has three key elements: international portfolio funding (FPI) at $800 billion, international direct funding (FDI), together with each listed and unlisted capital, at near $1 trillion, and $700 billion in exterior business borrowings. This brings the overall repatriable capital inventory to $2.5 trillion, whereas foreign exchange reserves – internet of RBI’s ahead quick positions – stand at $560 billion.

India has seen exits from each FPIs and FDI. Companies like Whirlpool and Hyundai are decreasing their holdings in Indian arms as a consequence of excessive valuations. In the monetary sector, Prudential is trying to promote its stake in Prudential ICICI AMC by a proposal on the market.

“This $2.5 trillion has the potential to leave. Of course, not all of it will, but could 5% exit? Could $100 billion flow out in a year? We have seen that happen before. In such a scenario, two things could happen – RBI depletes its reserves, or the rupee weakens. I believe we could see a mix of both outcomes.”

Kotak burdened the necessity for a strategic response. “The decision lies between tightening domestic liquidity or allowing the rupee to depreciate. What should our national strategy be? How should we approach this challenge? Our policymakers – including the finance ministry, RBI, and Sebi – must develop a cohesive strategy to counter this ‘vacuum cleaner’ effect.”