Now Reading: ITAT rules in Shah Rukh favour, quashes reassessment process | India News

-

01

ITAT rules in Shah Rukh favour, quashes reassessment process | India News

[ad_1]

MUMBAI: Superstar Shah Rukh Khan secured a major victory because the Income Tax Appellate Tribunal (ITAT) dominated in his favour, quashing reassessment proceedings and order initiated by the tax authorities for the 2011-12 monetary yr.

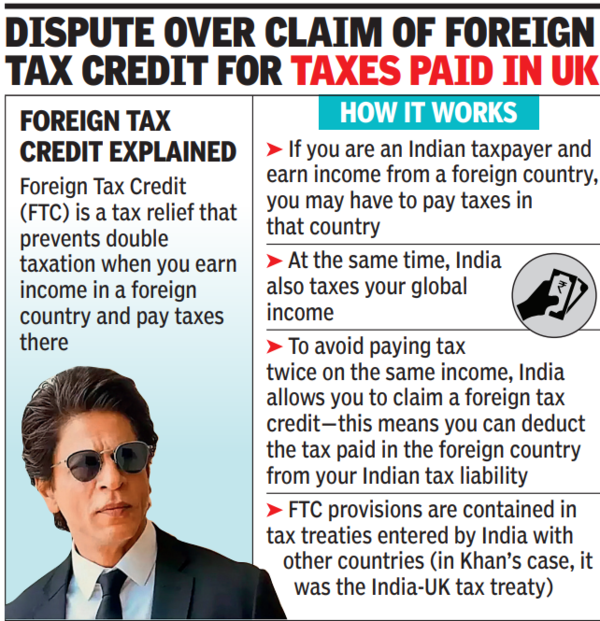

Against an earnings of Rs 83.42 crore declared by the actor in his income-tax (I-T) return, the tax officer denied his claims for international tax credit score (for taxes paid in the UK) and reassessed the earnings as Rs 84.17 crore. Such reassessment was executed past 4 years from the top of the related evaluation yr (2012-13).

The ITAT bench held that reassessment of the case by the income-tax division was not legally justified, marking an important win for the actor in his extended battle over international tax credit score claims.

The litigation associated to taxation of Khan’s remuneration for the film ‘RA One.’ As per the settlement between the actor and Red Chillies Entertainments (a movie manufacturing and distribution firm based by Khan), 70% of the movie’s taking pictures was to happen in the UK and subsequently 70% of the earnings would accrue abroad (which might be topic to UK tax together with withholding tax). The actor’s remuneration, in this regard, was routed by Winford Production, a UK entity. Tax authorities contended that such an association of fee, induced a income loss to India. The I-T officer denied the actor’s declare for international tax credit score, that was made in his authentic I-T return.

An Indian resident taxpayer is topic to tax in India on his/her world earnings. In easy phrases, international tax credit score provisions contained in tax treaties, allow an Indian taxpayer to deduct tax paid in the international nation from his India tax legal responsibility. This prevents double taxation of the identical earnings.

In an in depth order, the ITAT bench composed of Sandeep Singh Karhail and Girish Agrawal, dominated that the reassessment proceedings have been invalid. The tribunal famous that the assessing officer had did not show any recent tangible materials warranting a reassessment past the four-year statutory interval. It additional noticed that the disputed challenge had already been examined throughout the preliminary scrutiny evaluation of the case.

Citing a number of judicial precedents, the tribunal emphasised that reassessment beneath Section 147 could be executed after the expiry of 4 years from the top of the related evaluation yr, provided that sure circumstances have been met. For occasion, if the earnings had escaped evaluation on account of taxpayer’s failure to file an I-T return, or reply to a discover. Or, if the tax taxpayer had failed to totally and really disclose all materials details throughout the authentic evaluation. The tribunal discovered no proof of such failure on Khan’s half.

The ITAT bench concluded that the re-assessment proceedings have been unhealthy in regulation on a couple of depend and weren’t in conformity with the provisions of Section 147, and quashed the identical. Tax consultants consider that the judgment strengthens the place of Indian taxpayers with abroad earnings, reaffirming that reassessments can’t be arbitrarily initiated with out enough grounds.

[ad_2]